Health Insurance

Convalescence Benefit in Health Insurance

Key Features

Protecting You From the Financial Burden of Critical Illness

Coverage Highlights

Get comprehensive coverage for your health

Sum Insured as per Severity

The claim disbursal will be as per the severity of the disease covered under the policy

Extensive Critical Illness Coverage

Get coverage for 43 critical illnesses as per policy terms

Wide Sum Insured (SI) Options

Choose adequate sum insured from 5 lacs to 5 crores that suits your need

Lump Sum Payout

Get a lumpsum payout regardless of treatment costs

Lifetime Renewal

Option to avail lifetime renewal services (applicable for continuous coverage)

Flexible Usage

Avail the payout amount as needed for treatment, medication, or rehabilitation

Design Your Own Plan

Option to choose from 5 types of covers that best suits your needs

Note

Please read policy wording for detailed terms and conditions

Inclusions

What’s covered?Cancer Care

Covers critical illness as per category A (25%) and category B (100% sum assured)

Cardiovascular Care

Covers critical illness as per category a (25%) and category B (100% sum assured)

Kidney Care

Covers critical illness as per category A (25%) and category B (100% sum assured)

Neuro Care

Covers critical illness as per category A (25%) and category B (100% sum assured)

Transplant Care & Sensory Organs Care

Covers critical illness as per category A (25%) and category B (100% sum assured)

Note

Please read policy wording for detailed terms and conditions

Exclusions

What’s not covered?Waiting Period

Critical illness diagnosed within the first 180/ 120 days is excluded unless coverage is renewed without a break as per the policy terms

Sexually Transmitted Diseases

Treatment for sexually transmitted diseases are not covered

Birth Defects

Expenses for treatment of birth defects and congenital anomalies

War and Related Activities

Expenses incurred due to war, invasion, civil war, rebellion, and related events stays

Natural Perils

Storms, earthquakes, volcanic eruptions, and other natural hazards are not covered

Self-inflicted Injuries

Self-inflicted injuries, suicide attempts, insanity, and illegal acts are not covered

Intoxicating Substances

Coverage for treatment required after misuse of drugs and alcohol (except narcotics used under medical direction)

Note

Please read policy wording for detailed terms and conditions

Additional Covers

What else can you get?Cancer Reconstructive Surgery

Additional sum assured for reconstructive surgery if a category B cancer claim is accepted

Cardiac Nursing

Additional sum assured for cardiac nursing if a category B cardiovascular claim is accepted

Dialysis Care

Additional sum assured for dialysis if a category B kidney care claim is accepted

Physiotherapy Care

Additional sum assured for physiotherapy if a category B neuro care claim is accepted

Sensory Care

Additional sum assured for speech therapy or hearing loss treatments (e.g., cochlear implants) if a category B sensory organs care claim is accepted

Benefits You Deserve

Flexible Sum Insured Options

Sum Insured options of INR 1Lac- to INR 50Lacs

Tax Benefits

Deductions under Section 80D

Lifetime Renewal

Lifetime renewal option is available for continuous coverage

Beyond Hospital Bills: A Complete Guide to Convalescence Benefits in Medical Insurance

Recovering from a major illness or surgery is rarely just about the hospital stay. The real challenge often begins after the discharge. When you are back home, unable to work, and still incurring costs for special diets, nursing, or household help, the financial strain can feel heavier than the medical bills themselves.

This is where a lesser-known but highly valuable feature of health insurance comes in, which is the convalescence benefit in health insurance.

Convalescence Benefit in Health Insurance Meaning

In simple terms, your health insurer pays convalescence benefit as a lump-sum amount if your hospitalisation exceeds a specific number of days. People often refer to the term as recovery benefit or recuperation benefit as well.

Unlike your standard health insurance coverage, which reimburses specific medical bills, the convalescence benefit is a fixed payout.

The insurer does not require bills regarding how you spent this money. The insurer gives you an 'allowance' because it recognises that prolonged hospitalisation leads to financial loss beyond just medical bills.

The key features are:

1. Insurers don't pay this for every hospitalisation. It will only kick in if you are admitted to the hospital for a specified and continuous period of time.

2. You can't choose the convalescence benefit. Insurers provide a pre-defined sum or a percentage of the sum insured as the benefit.

3. It is not the same as the sum insured amount. Therefore, claiming this will not reduce your cover.

Convalescence Benefit vs Daily Cash Allowance: Differences Explained

Many people often get confused about the daily cash benefit and convalescence benefit. Although they both offer similar features, these two differ in the following ways:

Aspect | Convalescence Benefit | Daily Cash Benefit |

Eligibility Criteria | Prolonged hospitalisation more than 10 days* | Starts from day 1 of hospitalisation |

Payout | Lump-sum amount | Daily fixed amount |

Purpose | To cover post-discharge expenses | To cover daily expenses like food |

Amount | Starts from ₹5,000 | Starts from ₹500 |

Frequency of Pay | Once per policy year | Multiple days up to the specified limit |

*Note: This depends on the insurer and the type of policy. Check the brochure and policy wording for more details

Meet Our Expert For Assistance

Schedule your visit for personalised solutions and guidance that you can trust!

Why Insure Your Health with Bajaj General?

Buy Now

How Does Convalescence Benefit Work?

To understand how convalescence benefit in health insurance work, we need to look at the trigger period. This benefit is not intended for minor treatments, such as cataract surgery or a 2-day viral fever.

It is designed for serious ailments such as jaundice, accidents, or major surgeries, that keep you bedridden for over a week.

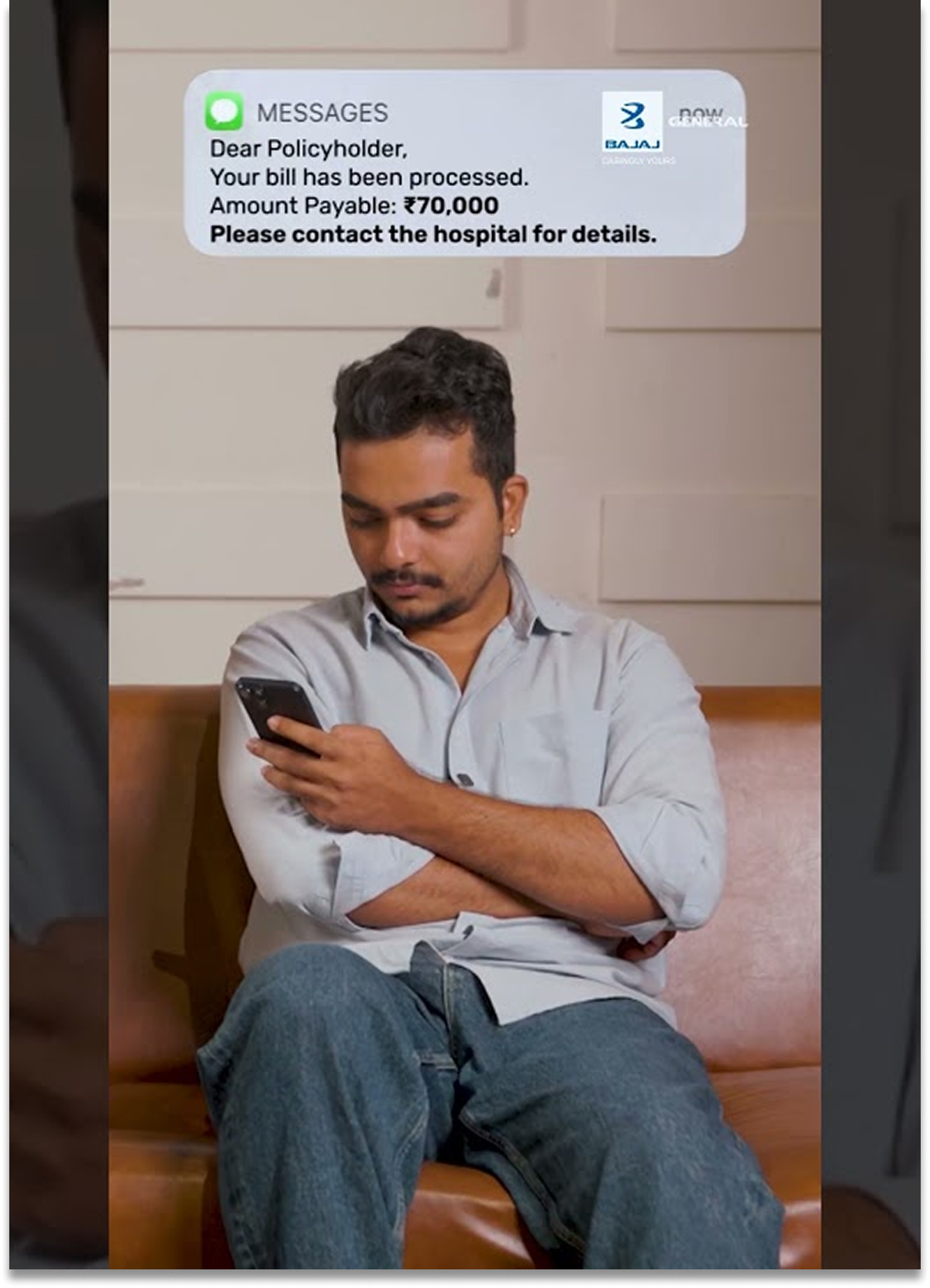

Let’s take the example of Ravi, a 35-year-old software engineer. He holds a Bajaj General Insurance Health Guard Policy. Unfortunately, he suffers from a severe case of typhoid and is hospitalised.

1. Scenario A (5 Days in Hospital): Ravi is discharged after 5 days. The insurance company pays for his medical bills, but he does not receive the convalescence benefit. This is because his stay was shorter than the policy's requirement (usually 10 days).

2. Scenario B (12 Days in Hospital): Ravi’s infection is severe, requiring a 12-day continuous hospital stay.

In this scenario, Bajaj General Insurance pays his hospital bill of ₹1.5 lakh directly via cashless settlement.

Since his stay (12 days) exceeded the trigger limit (10 days), he is eligible for the benefit. Bajaj transfers a flat ₹5,000* to his account.

Ravi uses this ₹5,000 to pay for the nutritious meals and supplements he needs for the next two weeks of rest at home. He does not need to submit bills for the fruits or supplements; the proof of his 12-day hospital stay is sufficient to release the payment.

*Note: This may depend on the sum insured amount or the specific policy. Please use discretion.

Which Health Insurance Plan Offers a Convalescence Plan?

Bajaj General Insurance has integrated this benefit into its flagship products, recognising that comprehensive protection goes beyond hospital bills.

Bajaj General Insurance Health Guard (Gold and Platinum Plans)

This is one of our most popular comprehensive plans. Along with being an all-rounder, Health Guard provides a convalescence benefit of ₹5,000 to ₹7,500 per policy year.

The benefit is applicable if the insured is hospitalised for a disease, illness, or injury for a continuous period exceeding 10 days. For families, this plan acts as a financial cushion. If the primary breadwinner is hospitalised for two weeks, this payout acts as a mini-income replacement.

Download Policy Documents

Get instant access to policy details with a single click

Step-by-Step Guide

To guide you through your insurance journey.

How to Buy

-

1

Visit Bajaj General website

-

2

Enter personal details

-

3

Compare health insurance plans

-

4

Select suitable coverage

-

5

Check discounts & offers

-

6

Add optional benefits

-

7

Proceed to secure payment

-

8

Receive instant policy confirmation

How to Renew

-

1

Login to the app

-

2

Enter your current policy details

-

3

Review and update coverage if required

-

4

Check for renewal offers

-

5

Add or remove riders

-

6

Confirm details and proceed

-

7

Complete renewal payment online

-

8

Receive instant confirmation for your policy renewal

How to Claim

-

1

Notify Bajaj General about the claim using app

-

2

Submit all the required documents

-

3

Choose cashless or reimbursement mode for your claim

-

4

Avail treatment and share required bills

-

5

Receive claim settlement after approval

How to Port

-

1

Check eligibility for porting

-

2

Compare new policy benefits

-

3

Apply before your current policy expires

-

4

Provide details of your existing policy

-

5

Undergo risk assessment by Bajaj General

-

6

Receive approval from Bajaj General

-

7

Pay the premium for your new policy

-

8

Receive policy documents & coverage details

How to Claim Convalescence Benefit From Bajaj General Insurance?

Claiming this benefit is simpler than a standard reimbursement claim because you don't need to collate dozens of pharmacy bills. The primary evidence required is proof of the duration of your stay.

Step 1: The discharge summary is the most essential. When the hospital discharges you, ensure your summary clearly mentions the admission and discharge dates. This document is the proof that your stay exceeded the 10-day limit.

Step 2: Inform us of your claim via our website or the Bajaj General app. You can do this simultaneously with your main hospitalisation claim.

Step 3: If you have already submitted documents for a cashless or reimbursement claim for the medical bills, you need to flag that you are eligible for the convalescence benefit. However, if you are claiming separately, then you should submit your KYC documents, cancelled cheque, claim form and discharge summary.

Step 4: Once our team verifies that the stay exceeded the required days, you will receive the fixed amount directly to your bank account.

Bajaj General Insurance makes sure that you are protected from all kinds of financial losses during your hospitalisation. Buy a comprehensive health insurance policy via the Bajaj General app and enjoy exciting benefits such as convalescence benefit.

Create a Profile With Us to Unlock New Benefits

- Customised plans that grow with you

- Proactive coverage for future milestones

- Expert advice tailored to your profile

Frequently Bought Together

View All

Quick Links

Diverse more policies for different needs

Insurance Samjho

Saving vs Medical Expenses

Is Health Insurance just an expense

MHCP EDGE +

Kitna Health Insurance Cover Enough Hai?

Home Insurance-All Risk Cover

Home Insurance-Long Term Cover

Home Insurance-No Content Declaration

Home Insurance-World Wide coverage

Take control of your digital security

Data Privacy Day | Bajaj General Insurance

Be Cyber Jagrook

Explore our articles

View All

Create a Profile With Us to Unlock New Benefits

- Customised plans that grow with you

- Proactive coverage for future milestones

- Expert advice tailored to your profile

What Our Customers Say

Highly satisfied

Clear policies, easy renewal, and great coverage options. Highly satisfied with this health insurance app.

Piyush Kumar

Mumbai

17th Mar 2025

Highly recommend!

Managing my health, vehicle & cyber insurance is so simple with this app. Highly recommend!

Pooja Kaushik

Vadodara

2nd Feb 2025

Simple, fast & effective!

A reliable health insurance app with all features in one place—simple, fast & effective!

Hrithik Mishra

Delhi

31st Jan 2025

Love this app!

Managing my family’s health insurance has never been this convenient. Love this app!

Shagun Gupta

Mumbai

31st Jan 2025

Reliable & affordable

Reliable & affordable medical insurance plan—gives complete health security for my family.

Shubham Singh

Delhi

30th Jan 2025

Financial convenience

Medical crises are stressful, but financial convenience is guaranteed by this health plan

Pushpendra Gurjar

Mumbai

30th Jan 2025

Great coverage options too!

Finding pregnancy health insurance was stress-free on Bajaj General app. Great coverage options too!

Rajesh Kumar

Mumbai

24th Jan 2025

User-friendly and efficient!

Securing my family's health with Bajaj General has been hassle-free. Their app is user-friendly and efficient!

Gautam Mongia

Delhi

24th Jan 2025

FAQ's

Is the Convalescence Benefit deducted from my Sum Insured?

No, in most modern plans such as Bajaj General Insurance Health Guard, the convalescence benefit is an over-and-above benefit. It does not reduce the sum insured available for your medical treatment.

Does this benefit cover day-care procedures such as dialysis or chemotherapy?

No, convalescence benefit strictly requires continuous hospitalisation (in-patient care) exceeding a set number of days (usually 7 or 10). Day-care procedures taking less than 24 hours do not qualify.

Do I Need to Survive for a Certain Period After Diagnosis to Claim the Benefit?

Yes. A 30-day survival period after diagnosis is mandatory.

Can I Buy the Critical Illness Plan Online Without Any Paperwork?

Yes. The entire purchase process is completely digital.

Is the Policy Document Sent Immediately After Online Payment?

Yes. The document is emailed instantly after successful payment.

Is There Any Medical Test Required Before Purchasing a Critical Illness Rider?

Medical tests may be required depending on age and health conditions based on underwriting guidelines.

Can I claim convalescence benefits for 2 different hospitalisations in the same year?

Usually, insurance companies cap this benefit at once per policy year per family or individual. If you are hospitalised twice for 11 days each, the insurer will likely provide the benefit only for the first instance. Check your policy wording for per-occurrence or per policy-year limits.

Can I Switch from Another Insurer to Bajaj General Insurance Without Losing Coverage?

Yes. Portability benefits allow switching without losing accrued benefits if done within guidelines.

Popular Search

With GST waiver, individual and family floater policies for health, personal accident, and travel insurance (on retail basis) are 18% cheaper from 22 September 2025. Secure what matters at an affordable price!