Motor Insurance

Standalone Own Damage Car Insurance

Get Up To 85% Off*

Stay protected on the road, no matter what comes your way

Coverage Highlights

Get comprehensive coverage for your car

Premium

Starting from INR 2094*

Cashless Garages

7,200+ network garages for hassle free services

Own Damage Cover

Covers damage to your car due to accidents, fire, theft and natural calamities

No Claim Bonus

Up to 50%

Optional Covers

Wide range of Add Ons

On The Spot Claim Settlement

You can instantly register your car insurance claim from the accident spot and get it settled within minutes through our Bajaj General App

24x7 Spot Assistance

Get 24x7 roadside assistance, ensuring help is always just a call away, no matter when or where your car breaks down

Inclusions

What’s covered?Accidents

Damages and losses that arise out of accidents and collisions

Natural or Man-Made Disasters

Damages and losses to car by events like floods, cyclones, earthquakes, riots or vandalism

Fire Damage

Damages and losses if your car catches fire or explodes

Theft

Financial losses when your car is stolen

In Transit Damage

If your car is damaged while being transported, this covers the repair costs

Exclusions

What’s not covered?Intentional Damage

Any damage caused to the car intentionally

Depreciation

Normal wear and tear of the car due to usage and depreciation in value is not covered

Mechanical or Electrical Breakdown

If your car suffers an electrical or mechanical breakdown, the cost of repairs would not be covered

Illegal Actvities

Any type of illegal activity such as driving without a license, under the influence of alcohol and/or drugs, or using the car for criminal activity

Geographic Limits

Your insurance policy is only valid within India. If your vehicle meets with an accident outside the country, your claim will be rejected.

Commercial Use

Using private car for commercial purposes like delivery or ridesharing without proper coverage

Note

Please read policy wording for detailed exclusions

Additional Covers

What else can you get?24x7 Road Side Assistance

Provides immediate roadside help for emergencies like flat tyres, towing, fuel assistance and more

Consumable Expenses

Coverage for consumables items like grease, lubricants, engine oil, oil filter, brake oil, etc

Zero Depreciation Cover

Every year the value of a car depreciates but with zero depreciation cover, there are no depreciation cuts even when you make a claim, and you get the entire amount in your hands

Pay As You Consume

If you drive less then you can pay less by selecting number of kilometers driven in a year and thus saving on your insurance premium

No Claim Bonus Protector

Protects your No Claim Bonus even if you make a claim ensuring you get discount on your premium

Tyre Safeguard

This add-on cover can be fruitful if your car's tyre or tube gets damaged due to an accident. Tyre secure cover provides coverage for replacement expenses of tyres and tubes of the insured vehicle

Conveyance Benefit

If your car is in the garage for repairs, this cover will pay for money spent on cabs for your daily commute

Engine Protector

Covers financial losses incurred due to damage to your car engine

Vehicle Replacement Advantage

Recover invoice value of your car back in case of theft or total loss

Benefits You Deserve

Reliable Customer Support

We have a dedicated call centre and chat support taking care of all your needs

7200+ Cashless garages

Wide network of cashless garages for hassle free service

On the Spot Claim Settlement

Register claim on accident spot and get it settled within minute on our app

Get Best Protection For Your Vehicle | Standalone Own Damage Car Cover

A standalone own damage policy, as the name suggests, protects your car from unexpected financial burdens that your vehicle may face. This includes theft, damage from natural disasters, vandalism, or accidental damage.

It also protects your investment from going into complete waste (total loss) by paying the IDV of your vehicle. So, even if you lose your vehicle in an accident, you don’t have to worry about loss.

Bajaj General Insurance provides a customisable and robust standalone own damage policy so that you can rest assured. Let’s dive in below!

What are the Features of a Standalone Own Damage Policy?

Understanding the coverage details of the Standalone Own Damage Cover is crucial to making an informed decision. The table below provides a clear overview of what is covered under this policy:

Coverage Type | Description |

Accidental Damage | Covers repair costs for damages due to accidents. |

Theft | Provides compensation if the vehicle is stolen. |

Fire and Explosion | Covers damages caused by fire, explosion, or self-ignition. |

Natural Calamities | Protection against damage from floods, earthquakes, storms, etc. |

Man-made Disasters | Covers damages due to riots, strikes, or malicious acts. |

Personal Accident Cover | Offers financial protection in case of injury or death of the owner-driver. |

At-A-Glance

Compare Insurance Plans Made for You

| Feature |

Third Party Liabilty Cover |

Own Damage Cover |

Comprehensive Car Cover |

Comprehensive Cover with Add-ons |

|---|---|---|---|---|

| Overview | Covers legal liabilities arising due to body injury or property damage to others due to your car. It is mandatory by law. | Covers expenses arising out of damage to your car. | Full fedged cover comprising of Third Party Liability cover and Own Damage covers | Enhance coverage by opting for various Add-ons over and above the comprehensive cover |

| Policy Period | 1 or 3 years | 1 Year | 1 and 3 years | 1 and 3 years |

| Third Party Liability for Injury, Death & Property Damage | Yes | No | Yes | Yes |

| Accidents & Collisions | No | Yes | Yes | Yes |

| Natural or Man-Made Disasters | No | Yes | Yes | Yes |

| Fire Damage | No | Yes | Yes | Yes |

| Theft | No | Yes | Yes | Yes |

| Compulsory Personal Accident | Yes | Yes | Yes | Yes |

| Add-on: No Claim Bonus | No | No | No | Yes |

| Add-on: Zero Depreciation Cover | No | No | No | Yes |

| Add-on: Lock & Key Replacement | No | No | No | Yes |

| Add-on: 24x7 Roadside Assistance | No | No | No | Yes |

| Add-on: Consumables Cover | No | No | No | Yes |

| Explore more add-ons | No | Up to 27 Add Ons | Up to 27 Add Ons | Up to 27 Add Ons |

What is the Difference Between Standalone Own Damage and Comprehensive Vehicle Insurance?

Aspect | Standalone Own Damage Policy | Comprehensive Policy |

Scope of Coverage | Provides complete coverage for any damage your vehicle sustains | Covers the damages to your vehicle and third-party liabilities |

Legal Status | Optional | Optional, but it includes mandatory third-party insurance |

Premiums | Lower, since it covers only one type of risk | Higher as it provides coverage for third-party and own damage |

Who Needs It | For people who want to ensure that their car is covered for own damage | For people looking for a single plan who want to extend their coverages caused by own damage and to third party |

Add-Ons | Available | Available |

As you can see, comprehensive coverage covers all kinds of damage.

You should buy Standalone own damage cover when you already have a third-party insurance. It acts as an extra layer of protection.

What Benefits Does Bajaj General Insurance’s Own Damage Coverage Provide?

The benefits of opting for a Standalone Own Damage Cover from Bajaj General Insurance are numerous. This section outlines the advantages that policyholders can enjoy.

1. Comprehensive Protection: Covers damages due to accidents, theft, natural calamities, and man-made disasters.

2. Flexible Add-ons: Options to include add-ons like zero depreciation, engine protector, and roadside assistance.

3. No Claim Bonus (NCB): Enjoy discounts on premiums for claim-free years.

4. Cashless Repairs: Access to a wide network of cashless garages across the country.

5. Quick Settlement: Fast and hassle-free claim settlement process.

6. Financial Security: Protects you from unexpected repair costs, ensuring peace of mind.

7. Customizable Plans: Tailor the policy with add-ons to suit your specific needs.

8. Wide Network: Access to numerous cashless garages for convenient repairs.

9. Enhanced Protection: Provides coverage beyond the basic third-party liability insurance.

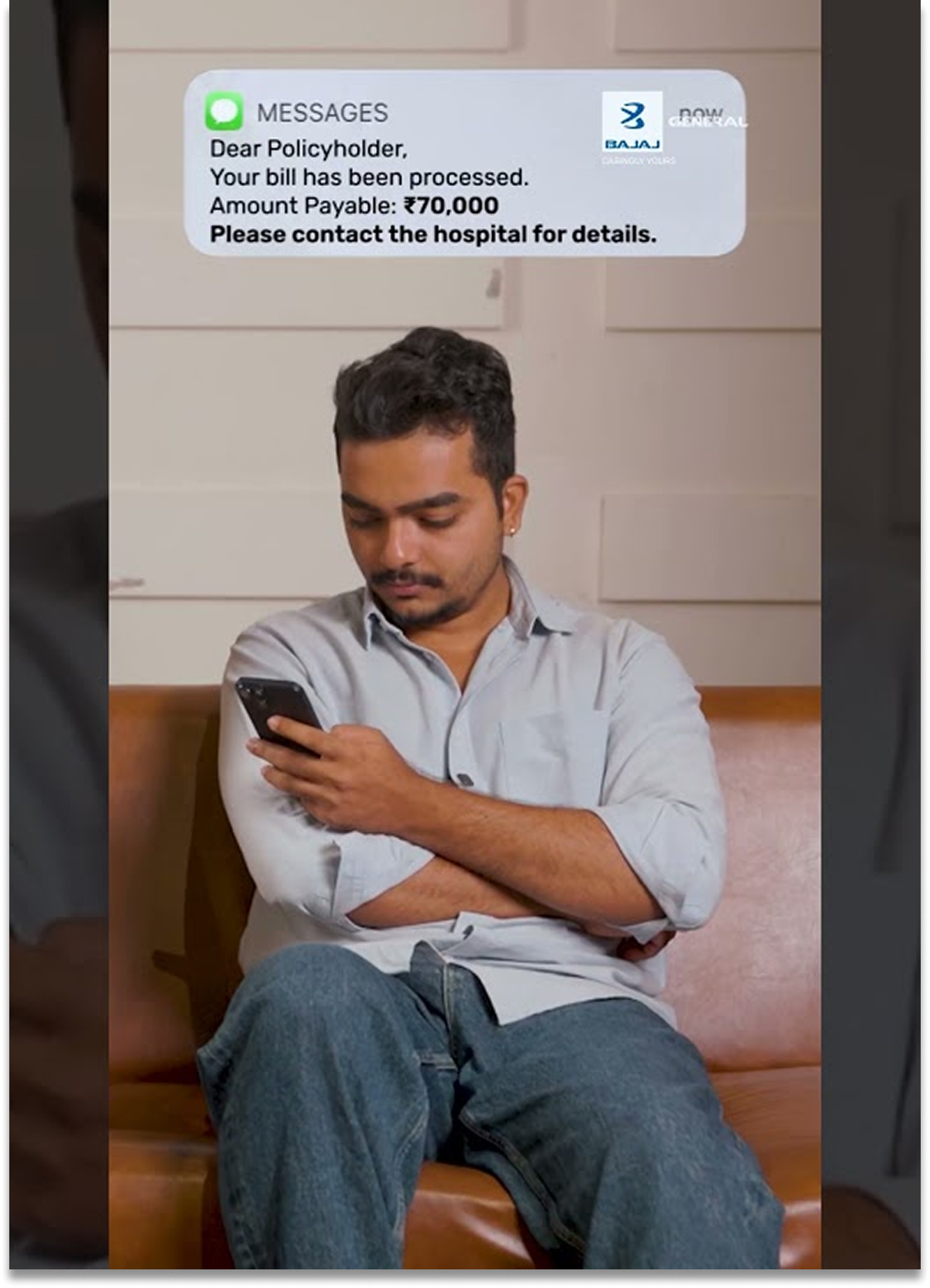

What is a Real-Life Example of Own Damage Policy in Action?

According to a recent report by The Times of India, a car was badly damaged after skidding off the Delhi-Mumbai Expressway near Nuh. Thankfully, the 5 people inside the car made it out safely. But their car was damaged beyond recognition.

Now, normally, they would've suffered a total loss with just a third-party insurance since they didn’t damage anyone else’s property. But with a standalone own damage policy, they can recover their expenses up to a limit.

They have to raise a claim to their insurer and inform them about the incident. After that, the insurer will check the damage and send them a claim amount. If they agree, then they will receive the amount in their bank account.

Dos and Don’ts of Purchasing a Standalone Own Damage Policy for Your Vehicle

Did you know, according to Mordor Intelligence, India’s motor insurance market is growing at a rate of 9.59% CAGR. Experts believe that the market will reach a valuation of USD 14.82 million by 2030.

This showcases the growing need for people in India to buy private car insurance policies such as standalone OD cover. But before you go along with the trend, here are some checklists that you should keep in mind:

Dos of Standalone Own Damage Private Car Policy

1. Compare Policies Online: Before buying the first policy that shows up in your search, wait. Check different policies online. Bajaj General has a robust comparison tool that helps you compare various plans to help you make an informed decision.

2. Disclose Accurate Information: Before you buy, make sure you input all information about your vehicle, driver and yourself correctly. If you have some modifications on your car, you should disclose them to your insurer for a hassle-free claim process.

3. Check the Insurer’s CSR: Claim settlement ratio (CSR) is a crucial indicator of whether you can trust an insurer. Choose a provider who has a high CSR percentage, such as Bajaj General Insurance.

4. Ensure a Valid TP Coverage: Before you buy a standalone own damage coverage, make sure that you have an active and valid TP policy. This is because OD acts as a supplementary coverage to your mandatory TP policy.

5. Check the IDV: Insured declared value, or IDV, plays an important role in deciding your premium. Although everyone wants a low premium, it can mean that your IDV might be low. Therefore, choosing the correct IDV is necessary.

Don’ts of Standalone Own Damage Policy

1. Don’t Make Minor Claims: Claims for minor repairs may seem convenient, but can cost you your no-claim bonus (NCB). A no-claim bonus can give you discounts on your premium if you maintain a claim-free year.

2. Don’t Buy a Cheap Policy: Getting the lowest possible plan is not the right choice. It may not contain valuable coverage and may leave you uncovered in unexpected situations.

3. Don’t Drive Without a License: Driving without a license is illegal, and if something happens during your drive, you will be uncovered. This is because insurers will not cover you if you are not following the traffic rules.

4. Don’t Use a Private Car for Professional Use: If your car is registered as a personal car, then you must not use it for commercial use. If you do so, your claim may be rejected.

Why Buy Motor Insurance from Bajaj General?

Buy Now

Why Choose Bajaj General Insurance for Your Standalone Own Damage Cover?

Choosing Bajaj General Insurance for your standalone own damage policy (OD) cover ensures your vehicle is protected by one of the most trusted names in the Indian insurance industry. Our OD policy is designed to offer financial security against accidents, natural calamities, and theft, backed by a seamless digital experience.

1. Cashless Claims: Access a vast network of over 7,200+* authorised garages across India, allowing for hassle-free repairs without out-of-pocket expenses.

2. High Settlement Ratio: Benefit from a streamlined, transparent claims process known for its industry-leading speed and reliability.

3. Customisable Add-ons: Enhance your basic OD cover with powerful riders like Depreciation shield for Zero Depreciation, Engine Protector, and 24 X 7 Spot Assistance for 24*7 Roadside Assistance for comprehensive peace of mind.

4. Instant Policy Issuance: Purchase or renew your cover online in minutes with minimal documentation.

With 24/7 customer support and a reputation for caringly yours service, we ensure that even in the event of a mishap, your journey back to the road is smooth and stress-free.

*Note: Subject to change.

What is the Role of IDV in a Standalone Own Damage Policy?

In Standalone Own Damage (OD) motor insurance, the Insured Declared Value (IDV) serves as the sum insured. This means it is the maximum financial liability the insurer will undertake. Unlike Third-Party insurance (TP), which covers legal liabilities to others, the OD component focuses on your vehicle's protection, making the IDV the most critical factor in your policy.

The primary role of IDV is to establish the current market value of your vehicle. It is calculated by taking the manufacturer's listed selling price and adjusting it for age-based depreciation. For a brand-new car, the IDV is typically 95% of the ex-showroom price.

Main Functions of IDV:

1. Claim Ceiling: In cases of Total Loss (theft or damage beyond 75% of the IDV), the insurance company pays this fixed amount as compensation.

2. Premium Determinant: The IDV is the base figure used to calculate your own damage premium. A higher IDV provides better coverage but results in a higher premium, while a lower IDV reduces your yearly cost but leaves you underinsured.

3. Constructive Total Loss (CTL) Benchmark: If repair costs exceed 75% of the IDV, insurers declare the vehicle a total loss and pay out the full IDV.

Accurately declaring your IDV ensures you receive a fair payout that reflects the true value of your asset without overpaying on premiums.

What is the Depreciation Rate for Your Vehicle?

Age of Vehicle | % of Depreciation for Fixing IDV |

Not exceeding 6 months | 5% |

Exceeding 6 months but not exceeding 1 year | 15% |

Exceeding 1 year but not exceeding 2 years | 20% |

Exceeding 2 years but not exceeding 3 years | 30% |

Exceeding 3 years but not exceeding 4 years | 40% |

Exceeding 4 years but not exceeding 5 years | 50% |

Apart from the depreciation rate for your car, your car and bike parts face separate depreciation rates. These rates, fixed by IRDAI, include:

Material Parts | Depreciation Rates |

Fibreglass Components | 30% |

Paintwork | 50% of material cost |

Glass Parts | 0% |

Plastic Parts | 50% |

Rubber/ Nylon/Batteries | 50% |

So, when you claim repair, keep these rates in mind, as the insurer will only pay the amount minus depreciation.

What Factors Affect the Premium of a Standalone Own Damage Policy?

While third-party insurance premiums are fixed by the IRDAI based on engine capacity, the premium for a standalone own damage (OD) policy is determined by the insurer based on the level of risk they are taking. Several dynamic factors influence this cost:

1. Insured Declared Value (IDV): As the sum insured, the IDV is the biggest premium driver. A higher IDV (for newer or luxury cars) leads to a higher premium, while a lower IDV for older vehicles reduces the cost.

2. Vehicle Age and Depreciation: Newer cars have higher market values and more expensive spare parts, commanding higher premiums. As the vehicle ages, depreciation reduces the IDV and the corresponding premium.

3. Make, Model, and Fuel Type: High-end luxury cars, SUVs, and performance vehicles have higher repair costs and thus higher premiums. Additionally, CNG or Diesel variants often attract a slightly higher premium than Petrol models due to their higher initial cost.

4. No Claim Bonus (NCB): This is a powerful discount (ranging from 20% to 50%) earned for every claim-free year. It directly reduces the OD premium upon renewal.

5. Geographical Location: Vehicles registered in Zone A (metropolitan cities like Delhi or Kolkata) typically face higher premiums due to increased risks of accidents and theft compared to Zone B areas.

6. Add-on Covers: Choosing riders like Zero Depreciation or Engine Protect adds to the base premium but provides enhanced security.

How Do Insurers Calculate the Premium for a Standalone Own Damage Policy?

Let’s look at the formula for calculating the premium:

Own Damage Premium = (IDV × Premium Rate) + Cost of Add-ons – (NCB + Applicable Discounts)

For example, if your IDV is ₹10 lakh, the premium rate is 2%, the add-ons cost is ₹5,000, and you have an NCB of 15%, then your approximate premium will be:

(₹10 lakh x 0.02) + ₹5,000 - (15% + ₹1,000) = ₹20,000 + ₹5,000 - (20%+1,000) = ₹23,800 (approximately).

This is a tentative premium amount and can vary according to different insurers. You can use an online calculator for accurate premium estimates.

Note: This information is general and may not represent Bajaj General Insurance’s premium calculation methods. Please use discretion.

How Can You Port Your Standalone Own Damage Policy to Bajaj General Insurance?

Step 1: Initiate the Switch

Visit the Bajaj General Insurance’s official website or mobile app at least 45 days before your current policy expires to ensure a seamless transition without a coverage gap.

Step 2: Enter Vehicle Details

Next, you need to provide your vehicle registration number, make, model, and manufacturing year. Ensure you have your current policy details and third-party policy information handy.

Step 3: Customise Your Cover

Select your preferred Insured Declared Value (IDV) and choose from Bajaj’s range of add-ons, such as Depreciation shield for Zero Depreciation or Engine Protector.

Step 4: Declare Your NCB

Now, you need to input the No Claim Bonus percentage earned from your previous insurer. Bajaj General Insurance will verify this with your previous provider to apply the discount to your new premium.

Step 5: Inspection (If Required)

If your previous policy has already expired, Bajaj General Insurance may ask for a quick vehicle inspection either online or offline.

Step 6: Payment and Issuance

Complete the premium payment online through UPI, credit/debit or Netbanking. Once processed, your new Standalone OD policy document will be issued instantly and sent to your email.

Motor & Health Companion

Drive Confidently with Bajaj General

Experience seamless vehicle management with the Bajaj General Drive Smart App, featuring on-road assistance, fuel efficiency stats, driving alerts, and more

Track, Manage & Thrive with Your All-In-One Health Companion

Discover a health plan tailored just for you–get insights and achieve your wellness goals

Take Charge of Your Health & Earn Rewards–Start Today!

Be proactive about your health–set goals, track progress, and get discounts!

Frequently Bought Together

View All

Download Policy Document

Get instant access to your policy details with a single click.

Step-by-Step Guide

To help you navigate your insurance journey

How To Buy

-

1

Download the Bajaj General App from App stores or click "Get Quote"

-

2

Register or log in to your account.

-

3

Enter your car details

-

4

You will be redirected to the Car Insurance Page.

-

5

Ensure to check your No Claim Discount

-

6

Choose right Insured Declared Value (IDV) that reflects your car value

-

7

Evaluate Covers, Add Ons, Optional Covers and Exclusions

-

8

Select a plan from the recommended options, or customize your own plan

-

9

Review the premium and other coverage details

-

10

Proceed with the payment using your preferred method

-

11

Receive confirmation of your purchased policy via email and SMS

How To Renew

-

1

Login to the app

-

2

Enter your current policy details

-

3

Review and update coverage if required

-

4

Check for renewal offers

-

5

Add or remove riders

-

6

Confirm details and proceed

-

7

Complete renewal payment online

-

8

Receive instant confirmation for your policy renewal

How to Claim

-

1

Download our Bajaj General App on Android or iOS

-

2

Register or login to use Motor On the spot claim for a smooth process

-

3

Enter your policy and accident details (location, date, time)

-

4

Save and click Register to file your claim

-

5

Receive an SMS with your claim registration number

-

6

Fill in the digital claim form and submit NEFT details

-

7

Upload photos of damaged parts as instructed

-

8

Upload your RC and driving license

-

9

Receive an SMS with the proposed claim amount

-

10

Use the SMS link to agree/disagree with the claim amount

-

11

Agree to receive the amount in your bank account

-

12

Track your claim status using the Bajaj General App

Know More

-

1

For any further queries, please reach out to us

-

2

Toll Free : For Sales :1800-209-0144

-

3

Email ID: careforyou@bajajgeneral.com

What are the Required Documents for Porting to Bajaj General Insurance?

1. Copy of the previous year’s OD policy.

2. Copy of the active Third-Party insurance policy.

3. Vehicle Registration Certificate (RC).

4. NCB resignation/transfer certificate from the old insurer (if applicable).

Secure Your Valuable Asset Today!

So, what are you waiting for? Click on the ‘Buy Now’ button and generate a quote today. Download the Bajaj General app and keep track of your insurance today!

Quick Links

Diverse more policies for different needs

Insurance Samjho

Saving vs Medical Expenses

Is Health Insurance just an expense

MHCP EDGE +

Kitna Health Insurance Cover Enough Hai?

Home Insurance-All Risk Cover

Home Insurance-Long Term Cover

Home Insurance-No Content Declaration

Home Insurance-World Wide coverage

Take control of your digital security

Data Privacy Day | Bajaj General Insurance

Be Cyber Jagrook

Explore Our Articles

View All

Create a Profile With Us to Unlock New Benefits

- Customised plans that grow with you

- Proactive coverage for future milestones

- Expert advice tailored to your profile

What Our Customers Say

Great coverage option

Enjoyed a smooth motor insurance experience with Bajaj General app. Great coverage options!

Aryan Patil

Pune

19th Jan 2025

User friendly App

Bajaj General app simplifies the motor insurance process. Quick, efficient, and user-friendly! 🎯

Naadiya Rafiq

Mumbai

19th Jan 2025

Seamless Policy generation

Love the ease of getting motor insurance through Bajaj General App. Highly recommend! 🙌

Monu Dubey

Chennai

19th Jan 2025

Seamless Policy generation

Caringly Yours by Bajaj General offers a fast and secure motor insurance process. Highly efficient!

Rasool Rosi

Delhi

19th Jan 2025

User friendly App

The Bajaj General App is ideal for motor insurance. User-friendly and dependable! 🚗

Sam Shona

Mumbai

14th Jan 2025

Easy renewal

Need to renew motor insurance? Bajaj General App makes it an effortless task. 👍

Shan Qureshi

Delhi

11th Jan 2025

Seamless Experience

Bajaj General App makes motor insurance renewal easy. Just a few clicks, and you're covered! 🚙

Lakshay Dhariwal

Pune

11th Jan 2025

Economical coverages

Cool, fast, and economical motor insurance options available with Bajaj General. Fantastic experience with the app! 🚘

Biju VR

Bengaluru

23rd Dec 2024

FAQ's

What documents are required to purchase standalone motor insurance?

To purchase a motor insurance policy, you typically need to provide your vehicle's registration certificate, your driving license, proof of identity and address. Some insurers may also require additional documents, like a previous insurance policy, if you're renewing your policy with them.

Can I add multiple drivers to my motor insurance policy?

Yes, you can add multiple drivers to your motor insurance policy; however, coverage for additional drivers may vary based on the insurance provider. You will need to provide the necessary details of each driver, such as their name, age, and driving history. This may affect your premium depending on the risk profile of the additional drivers.

How do I update my vehicle details on my standalone own damage motor insurance policy?

To update your vehicle details on your motor insurance policy, such as a change in registration number or modifications to the vehicle, you need to inform your insurance provider. This can usually be done online through the insurer's website or mobile app, or by contacting their customer service.

What should I do if I lose my standalone own damage motor insurance policy document?

In case of document loss, contact your insurance provider immediately. Most insurers offer the option to download a duplicate copy from their website or mobile app. You may also request a physical copy to be mailed to you.

Who should buy a standalone own damage policy?

If you already have a third-party insurance, then you can get a standalone own damage policy. This provides extra protection for your car or bike, so you can rest assured. You can also buy it if you have a high-value vehicle or bike, such as a Lamborghini or a Harley-Davidson.

Can I drive without having my own damage coverage for my car?

Yes, you can drive without having your own damage car insurance policy, as it is not legally mandatory. But you must have a third-party vehicle insurance to stay legally compliant. Moreover, driving without own damage can prove to be risky.

What are the benefits of a standalone own damage policy?

Standalone own damage protects your vehicle from risky situations such as theft, fire or vandalism. It also covers repair costs if your car/bike gets damaged in an accident. With the right add-ons, it acts as an important financial tool for car or bike owners.

Can I transfer my existing motor insurance policy to the new owner?

Yes, you can easily transfer your vehicle's insurance to the new owner. The usual procedure for transferring vehicle insurance policy between two owners requires the new owner of the vehicle to submit an application form to the insurance provider within about 14 days of the registration transfer.

What risks are covered under an insurance policy for a vehicle?

The coverage for vehicle insurance can vary depending on the type of policy chosen. For instance, under third party insurance, you get coverage for third party liability, third party property damage, personal accident cover, etc. Similarly, comprehensive insurance covers own damage vehicle, theft, natural/manmade calamaties etc.

Why should I buy comprehensive vehicle insurance policy?

Investing in a comprehensive motor insurance is beneficial because it provides extensive coverage for your vehicle. There are certain add-ons for comprehensive motor insurance that can be added to give your vehicle an extra protection like damages for an accident, theft, natural disasters, damage to third party etc. as derived by the policy terms.

What is a Third-Party Liability Cover?

Third-Party Liability covers the legal liability one has to pay to the third party to whom damage is being caused. While opting for vehicle insurance, one has to choose between a comprehensive plan, which provides coverage for the policyholder and the third party, and a third-party policy, which provides coverage only for the third party.

Differenciate Third-Party Liability and Comprehensive Motor Insurance?

"Third-Party Liability: Covers damages you cause to another person or their property. It's mandatory by law. Comprehensive: Covers third-party liability plus damages to your own vehicle due to accidents, theft, natural disasters, etc. as per the policy terms"

How do I claim my own damage insurance?

Contact your insurer's toll-free customer service number or raise a claim through their website. You can also make a claim through their app. Bajaj General Insurance ensures that you get your claim raised within no time with their Bajaj General app.

Why does my vehicle insurance premium change during renewal?

Vehicle insurance premiums can change at renewal due to several factors, including depreciation, add-on covers, the type of model of your vehicle, and additional accessories. Consequently, the premium may increase or decrease each year.

How 'no claim bonus' is calculated at the time of renewal?

No claim bonus is calculated at renewal based on the consecutive years the insured has not filed a claim. The discount percentage usually increases each year, following the policy terms.

What is break-in insurance? What should I do in case of break-in?

The time gap between the policy expiration and the renewal of the policy is known as the break-in period. Your policy will remain inactive during this period. In case of a break-in, you are advised to renew your policy as soon as possible. You can complete the procedure online easily and your policy gets instantly activated.

When is vehicle inspection mandatory in motor insurance?

Usually, vehicle inspection occurs when purchasing a new vehicle insurance policy or during renewal process. Additionally, an inspection may be required when you file a claim for any damages, there is a change in the policy type, new accessories or equipment are added to the vehicle, or there is a change in ownership.

Can I change my motor insurance provider at renewal?

Yes, you can switch providers at renewal. Compare quotes and coverage options to find the best deal.

Why juggle policies when one app can do it all?

Download the App Now!

With GST waiver, individual and family floater policies for health, personal accident, and travel insurance (on retail basis) are 18% cheaper from 22 September 2025. Secure what matters at an affordable price!