Quick Overview on Health Insurance

-

1

Financial Protection Against Medical Costs: Health insurance helps manage unexpected healthcare expenses by covering hospitalisation, treatments and medical emergencies.

-

2

Wide Coverage Benefits: Plans offer coverage for ICU expenses, day-care treatments, ambulance services, AYUSH treatments and more.

-

3

Eligibility Criteria: Available for individuals aged 18 and above, with children eligible from 90 days.

-

4

Tax Benefits: Health insurance premiums can help reduce taxable income through eligible deductions under Section 126 of the Income Tax Act, 2025.

-

5

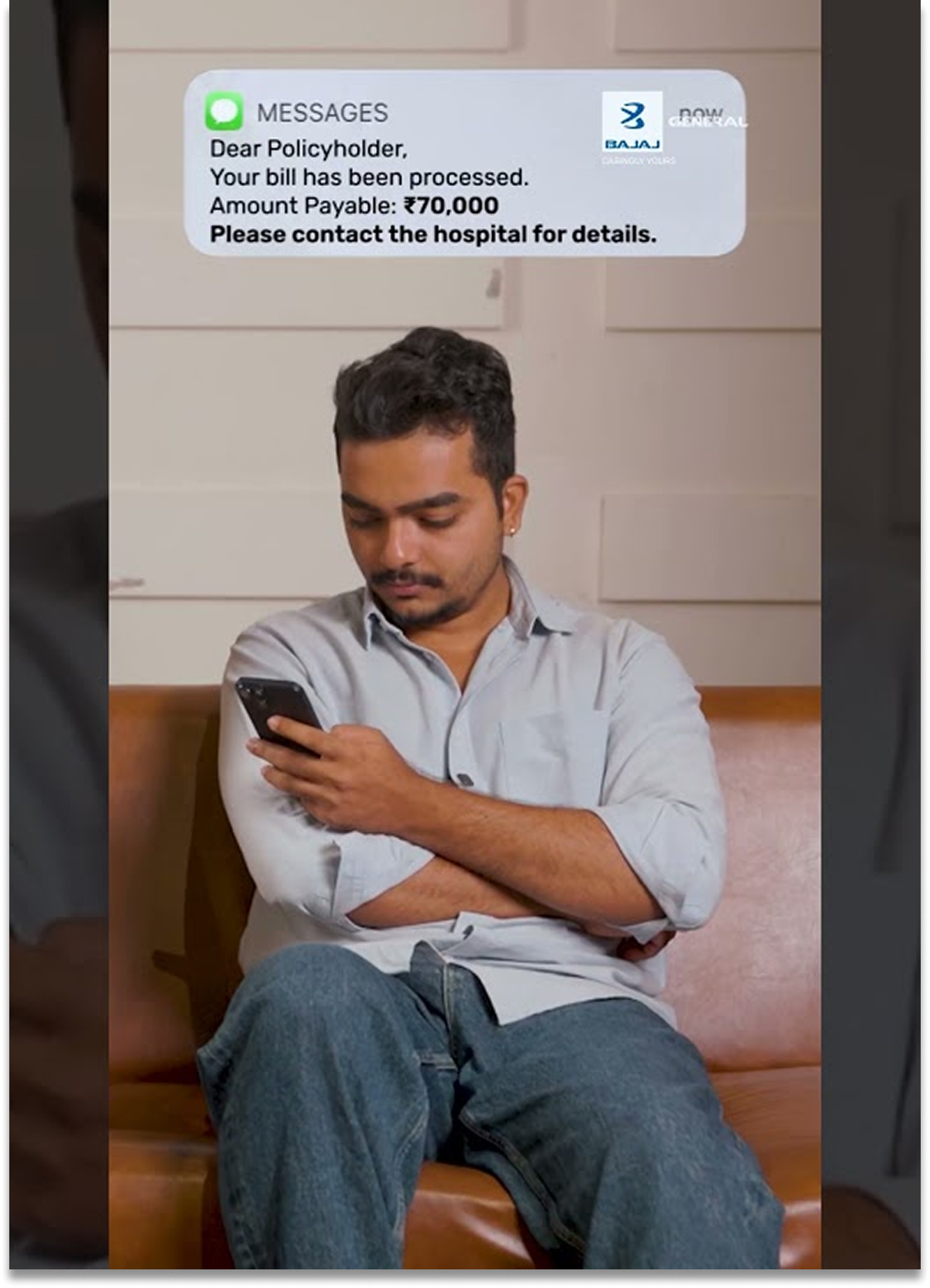

Claim Process: Claims can be settled through cashless or reimbursement options by submitting the required documents.

-

6

Factors to Consider: Evaluate factors like premium, sum insured, network hospitals, waiting periods, claim settlement process, inclusions, exclusions and add-on benefits to choose the right plan.