Health Insurance

Health Insurance for Parents

Personal health insurance for you

Comprehensive cover for all

Coverage Highlights

Key benefits

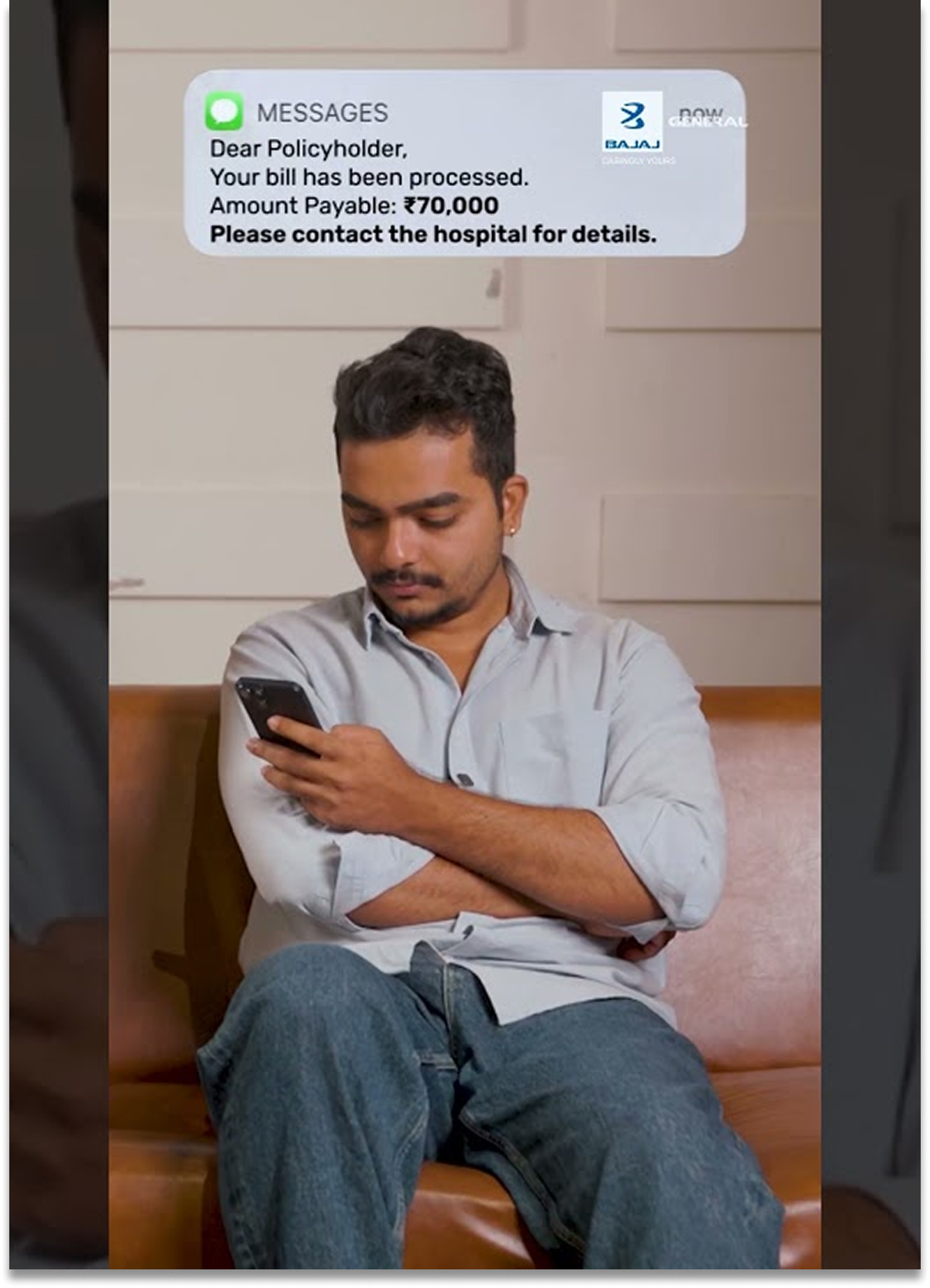

Cashless Treatment

The parents may also avail of the benefit of cashless health insurance in case they visit a network hospital to avail of the treatment. The insured just need to inform the insurance desk in the network hospital. The medical bills will be directly settled between the hospital and the insurance company. Having suitable medical insurance for parents ensures access to the cashless facility at over 800

Customize as Per Needs

The health requirements of every individual are different. Likewise, when it comes to parents their health condition also differs. Now you can opt for a mediclaim policy for parents and customize the plan as per the varying needs.

Hassle-free Claim Settlement

Our in-house claim settlement team ensures a quick, convenient and easy claim settlement process.

Tax Benefits

Under Section 80D of the Income Tax Act, the health insurance premium that is paid to parents is eligible for tax deductions. So, in case you are paying the premium for yourself and your parents who are below 60 years then the tax benefit limit upon the premium is Rs 50, 000. If the parents are 60 years of age and above, then the limit is extended up to Rs 75,000.

Know the Inclusions

Before you zero down any mediclaim policy, it becomes imperative to know the coverages offered under it. When you buy health insurance for parents online you can easily compare the features and benefits offered and make a decision. While buying a plan ensure that you look forward to coverages for daycare, critical illness, etc. The needs of every parent will differ at every stage of life. Hence, b

Key Inclusions

What’s covered?Hospitalization Expenses

Any expense incurred wherein the patient is hospitalized for a minimum of 24 hours consecutively except for certain procedures or treatments. A cover will not be provided if the admission is less than 24 hours.

Pre Hospitalization Expenses

A cover is provided for the medical costs incurred during the pre-defined number of days preceding the hospitalization of the person insured.

Post Hospitalization Expenses

A cover is provided for the medical costs incurred during the pre-defined number of days immediately after the insured person gets discharged.

Pre-existing Disease

In case any of the parents have a pre-existing ailment it will only be covered after the waiting period is completed. The waiting period differs from disease to disease and insurer to insurer. While buying a plan ensure that you check with the insurance company in regards to the waiting period under the specific parents health insurance.

Ambulance Cover

A cover is provided for the expenses incurred towards transferring to the hospital or between hospitals. This implies both the hospital's ambulance and the ambulance provided by the ambulance service provider up to a certain limit.

Modern Treatment Method

Modern treatment methods and advancements in technologies are restricted to 50% of the sum insured or up to Rs 5 lakh. It includes oral chemotherapy, intravitreal injections, bronchial thermoplasty, etc.*

Key Exclusions

What’s not covered?Any disease that is contracted during the initial days of the policy commencement

Any dental treatment that comprises dentures, dental implants, etc. unless as a result of accidental

Any medical expenses incurred due to invasion, war, etc.

Non-allopathic medicines

All costs incurred due to treating AIDS or any related disorders

Any treatment or ailment arising due to drugs or intoxication/alcohol

Cosmetic or plastic surgery

Additional Services

What else can you get?Hospitalization Expenses

Any expense incurred wherein the patient is hospitalized for a minimum of 24 hours consecutively except for certain procedures or treatments. A cover will not be provided if the admission is less than 24 hours.

Pre Hospitalization Expenses

A cover is provided for the medical costs incurred during the pre-defined number of days preceding the hospitalization of the person insured.

Post Hospitalization Expenses

A cover is provided for the medical costs incurred during the pre-defined number of days immediately after the insured person gets discharged.

Pre-existing Disease

In case any of the parents have a pre-existing ailment it will only be covered after the waiting period is completed. The waiting period differs from disease to disease and insurer to insurer. While buying a plan ensure that you check with the insurance company in regards to the waiting period under the specific parents health insurance.

Ambulance Cover

A cover is provided for the expenses incurred towards transferring to the hospital or between hospitals. This implies both the hospital's ambulance and the ambulance provided by the ambulance service provider up to a certain limit.

Modern Treatment Method

Modern treatment methods and advancements in technologies are restricted to 50% of the sum insured or up to Rs 5 lakh. It includes oral chemotherapy, intravitreal injections, bronchial thermoplasty, etc.*

Benefits You Deserve

Reinstatement Benefits

Unlimited reinstatement of the sum insured, even after its depletion.

Lifetime Renewal

Stay covered and renew yearly hassle-free!

No Medical Tests

Get instant cover; skip the tests if you are under 45!

Health Insurance for Parents: Ensuring Financial Stability and Quality Care

Rising medical costs and age-related health concerns make health insurance for parents a necessity, not a choice. A single hospital visit can disrupt years of savings, especially when senior care involves frequent treatments or emergencies. This is where the right cover comes in handy and makes sure that your parents get timely medical attention, access to quality hospitals, and financial stability when it matters most.

With healthcare expenses growing faster due to inflation, planning ahead becomes critical. A well-chosen policy safeguards both their health and your peace of mind. Let us explore why securing the right coverage for your parents is essential today.

Download Policy Document

Get instant access to your policy details with a single click.

Why Do You Need a Medical Health Insurance Plan for Your Parents?

Parents’ health needs demand careful financial planning. Medical costs in India have risen by around 14% annually in recent years, making unplanned hospital expenses difficult to manage. In these scenarios, a dedicated cover ensures timely treatment, access to quality hospitals, and financial stability during emergencies. Choosing a reliable health plan for parents also reduces the burden on family savings and long-term investments, especially during uncertain health situations.

Below are the direct benefits you can get from health insurance for parents:

1. Coverage for hospitalisation, including COVID-19 and other critical illnesses.

2. Cashless treatment at an extensive network of hospitals.

3. Protection of savings from high medical and ICU expenses.

4. Provision of better care options for parents above 50.

5. Faster, hassle-free claim settlements.

Plans such as Revised Health Guard offer sum insured options from ₹1.5 lakh to ₹50 lakh with policy terms of up to three years. These policies allow customisation based on medical needs, include tax benefits under Section 80D, and deliver strong coverage at cost-effective premiums. Selecting the best health insurance for parents ensures they receive consistent care without financial stress.

Save Tax with Parents' Health Insurance Policy

When you buy parents' health insurance in India, you can avail of *tax benefits under Section 80D. The benefits include deductions on single premium plans, senior citizen health insurance premiums, and preventive health check-ups.

To encourage people to choose parental health insurance, the Indian government offers various tax benefits on the health insurance premiums. Let us explore and understand the medical insurance for parents tax benefits under Section 80D one by one.

Tax Benefit on Single Premium Health Insurance Plan

The health insurance premium that is paid for a multi-year plan in a lump sum is entitled to a tax deduction under Section 80D. The tax-deductible sum is upon the total premium that is paid for the policy period. It is subject to the limits of ₹25,000 or ₹50,000, respectively.

Tax Benefit Upon Senior Citizen Health Insurance

Any individual who pays the health insurance premium for their parents can claim for tax deduction of up to ₹50,000. The tax deduction limit for the costs incurred on certain illnesses/ ailments for the elderly is up to Rs 1 lakh.

Deduction Upon Health Insurance Premium for the Parents

The costs incurred on preventive health check-ups are entitled to tax benefits. Most people are unaware of this aspect; the tax exemption limit for it is ₹5000.

The Deduction on Preventive Health Check-Ups

The tax exemption benefits are also extended to the OPD consultation and diagnostic centre expenses. A tax benefit can also be availed upon cash payment.

*The tax benefit for medical insurance for parents is subject to change as per the prevailing laws.

Why Insure Your Health with Bajaj General?

Buy Now

Why Should You Opt for Bajaj General Health Insurance Plans for Parents?

By understanding and choosing the right parents' health insurance plan, you can ensure their health needs are met without financial worries. When you decide to buy health insurance for parents in India, it’s important to compare different plans to find one that best suits your parents' specific healthcare needs.

The table below states the factors that will provide you with an edge if you purchase medical insurance for parents from Bajaj General Insurance:

Network Hospitals | 8000+ across the country |

Claim Process | Cashless and Reimbursement facility |

Health Administration Team | We have an in-house health administration team to expedite the health insurance claim process |

Health CDC (Claim by Direct Click) | An app-based feature that lets the policyholder keep track of the claims. The insured can make claims up to ₹20,000 easily |

Sum Insured | We offer multiple sum insured options. We have innovative packages to match individual needs |

Extensive Coverage | Comprehensive coverage for both planned and emergency hospitalisation based on the selected sum insured |

Top Up Plan | Enhance the coverage of the existing health insurance plan. It allows you to avail the benefits over and above the regular health insurance plan |

Add-on Cover | You may enhance the existing parental insurance by including add-on riders such as the Health Prime Rider, etc. |

Best Health Insurance Plans for Parents by Bajaj General Insurance

The table below shows the best health insurance for parents from Bajaj General Insurance that you may consider buying online for the secure future of your parents:

Plan Name | Entry Age | Plan Type |

Health Guard | 18 years to 65 years | Individual/Family floater |

Health Infinity | 18 years to 65 years | Individual policy |

Arogya Sanjeevani Policy | 18 years to 65 years | Individual/Family floater |

Critical Illness | 18 years to 65 years | Individual policy |

Premium Personal Guard | 18 years to 65 years | This is offered to only Risk Class- I, which includes administrative/ managing functions, doctors, accountants, architects, lawyers, teachers & likewise occupations |

Extra Care | 18 years to 70 years | Floater policy with a single premium for the family *The policy can be taken as an add-on cover to the existing hospitalisation–medical expenses policy |

Extra Care Plus | 91 days to 80 years | Floater policy *Additional coverage to the existing health insurance coverage |

M-Care | 18 years to 65 years | Individual and Floater policy |

Criti Care | 18 years to 65 years | Individual *This can be bought only offline |

Global Health Care | 18 years to 65 years | Individual |

Silver Health | 46 years to 70 years | Individual |

When is the Right Time to Buy Health Insurance for Parents?

Timing decides affordability and coverage strength. Earlier decisions deliver better outcomes.

You can buy health insurance cover for your parents during any of the following times:

Before 50

When you buy a policy before your parents turn 50, you lock in lower premiums and wider coverage choices. Insurers apply fewer restrictions at this age. You also complete waiting periods early, so your parents receive stronger coverage when age-related health issues start appearing.

At the Diagnosis Stage

If you buy health insurance for parents after a diagnosis, insurers often limit coverage. You may face higher premiums, longer waiting periods, or disease-specific caps. Buying earlier helps you avoid these restrictions and ensures your parents get broader protection when treatment becomes necessary.

Before Retirement

Once your parent retires, employer health cover usually ends. If you buy an individual policy early, you prevent coverage gaps and reduce reliance on savings. Moreover, you also avoid age-based loading and strict medical checks that raise costs later.

During Policy Review

When you review the policy annually, you keep coverage aligned with rising medical costs. With healthcare inflation at around 14%, you can not afford a policy lapse. So, you should upgrade the sum insured during renewals to avoid shortfalls during hospitalisation or long-term treatment.

With medical costs rising every year and age-related risks increasing, Bajaj General Insurance helps you secure timely health coverage for your parents before premiums rise and coverage options become limited. Get a quote today!

What is Health Insurance for Parents?

Health insurance for parents is designed to provide financial security against medical expenses. As parents age, they are more susceptible to health issues, making parents' medical insurance crucial. It covers hospitalisation, pre- and post-hospitalisation expenses, and other healthcare costs.

Types of Health Insurance for Parents

When it comes to health insurance for parents, take a look below to understand the types of coverage that can be availed for them:

Individual Health Insurance

As the name suggests, individual health insurance is a type of plan wherein the proposer and family members are covered in the same plan. So, if you plan to insure your parents, the sum insured will be separate for each and not shared. Our individual health insurance plan offers multiple sum insured options, pre- and post-hospitalisation cover, daily cash benefit, etc. So, if you are looking forward to health insurance for parents above 60 years, you may consider opting for such a plan.

Family Floater Health Insurance

You may also include your parent who is less than 65 years of age under a family floater health insurance plan. A family health insurance plan allows for the inclusion of multiple members of the family within the same plan with a single premium. Under such a plan, the sum insured is shared by all family members. It offers a cover for daycare procedures, road ambulance cover, etc.

Senior Citizen Health Insurance

As the age of an individual increases, undoubtedly, the care expenses also increase manifold. If you have a senior citizen at your home, you must consider investing in a senior citizen health insurance plan. These are dedicated plan that caters to different health care needs. The Bajaj General Silver Health Plan* offers both cashless and reimbursement benefits for hospitalisation costs due to an illness/ mishap. Anyone between the ages of 46 and 70 years can avail of this plan.

Wellness Supervisor

Insurance benefits and rewards

Earn points for health activities and get benefits as premium discounts & policy upgrades. Improve your health to reduce claims & maximize benefits.

Complete health assessment and data integration

Start with a detailed health evaluation and sync your medical records & wearables for real-time data on activity, sleep & vital metrics.

Insurance benefits and rewards

Earn points for health activities and get benefits as premium discounts & policy upgrades. Improve your health to reduce claims & maximize benefits

Complete health assessment and data integration

Start with a detailed health evaluation and sync your medical records & wearables for real-time data on activity, sleep & vital metrics.

Step-by-Step Guide

To guide you through your insurance journey.

How to Buy

-

1

Visit Bajaj General website

-

2

Enter personal details

-

3

Compare health insurance plans

-

4

Select suitable coverage

-

5

Check discounts & offers

-

6

Add optional benefits

-

7

Proceed to secure payment

-

8

Receive instant policy confirmation

How to Renew

-

1

Login to the app

-

2

Enter your current policy details

-

3

Review and update coverage if required

-

4

Check for renewal offers

-

5

Add or remove riders

-

6

Confirm details and proceed

-

7

Complete renewal payment online

-

8

Receive instant confirmation for your policy renewal

How to Claim

-

1

Notify Bajaj General about the claim using app

-

2

Submit all the required documents

-

3

Choose cashless or reimbursement mode for your claim

-

4

Avail treatment and share required bills

-

5

Receive claim settlement after approval

How to Port

-

1

Check eligibility for porting

-

2

Compare new policy benefits

-

3

Apply before your current policy expires

-

4

Provide details of your existing policy

-

5

Undergo risk assessment by Bajaj General

-

6

Receive approval from Bajaj General

-

7

Pay the premium for your new policy

-

8

Receive policy documents & coverage details

Frequently Bought Together

View all

How to Choose the Best Health Insurance Plan for Parents

Parents always want the best for their children. So, as a child, it is your responsibility to choose the best health insurance for parents, too.

Wondering how to choose medical insurance for parents? Listed below are the parameters to make an informed decision and buy the best health insurance for parents:

Understand the Policy Wordings

Before you sign below the dotted lines, ensure that you understand the terms and conditions offered within the policy. The policy wording is crucial, so if you have any doubt or are unable to understand a certain terminology, take an understanding of the same. Assess your need and go with a parental insurance plan that fulfils your requirements and is pocket-friendly.

Extensive Coverage

With time, parents are more prone to various health risks. Henceforth, it's always suggested to opt for a high sum insured. Choose a comprehensive parents' medical insurance plan that offers an array of coverages. This ensures that the parents get the best medical treatment, and finances do not remain a barrier.

Entry Age

When buying health insurance for parents, make sure to have a look at the entry age. Certain plans offer entry ages between 18 years to 65 years, and 46 years and 70 years. If your parent is old, you may consider including them in senior citizen health insurance. You may go forward with a plan wherein the entry age is permitted at an advanced age. Also, there is no age cap with lifetime renewability.

Network Hospitals

In case you wish to avail a cashless facility, the treatment must be taken at any of the network hospitals. Moreover, it's suggested to go through the list of network hospitals that are associated with the insurance company. It is also better than the reputed hospitals in your nearby area, whichs are also listed. This becomes helpful and convenient in case of an emergency and avail of the maximum benefit of a parent's health insurance.

Compare Health Insurance Plans

When it comes to buying health insurance for parents, compare plans online. Make a decision based on assessing the features, benefits, add-ons, and premiums offered with a plan.

Waiting Period

When buying parents' health insurance, an important aspect to understand is the waiting period for pre-existing ailments. Depending upon the plan, the pre-existing illness may remain covered only after completing the waiting period. It is recommended to opt for a plan that offers a lower waiting period and likewise offers coverage for maximum ailments.

Coverage Depth

When you evaluate a policy, look beyond the sum insured. Check hospitalisation limits, ICU caps, and room rent rules carefully. Tight sub-limits often increase out-of-pocket costs during treatment. Many plans appear affordable but restrict ICU charges or specific procedures. You should assess the real coverage scope to ensure your parents receive quality care without financial gaps.

Claim Track Record

An insurer’s claim performance directly affects your experience during emergencies. Compare claim settlement ratios and average settlement timelines. Faster and smoother claim processing reduces stress when your parents need urgent care. For health insurance for parents, reliable claims matter far more than slightly lower premiums.

Room Rent Flexibility

Room rent limits influence overall hospital bills. When you choose a higher room category than allowed, linked expenses, such as doctor fees and ICU charges, rise proportionately. Plans without room category caps give you flexibility and protect you from unexpected billing escalations during hospitalisation.

Restoration Benefit

Automatic restoration refills the sum insured after a claim. This feature proves useful if your parents face multiple hospitalisations in a single policy year. Without restoration, one large claim can exhaust coverage and leave you financially exposed for subsequent treatments.

Lifetime Renewability

You should always confirm the lifetime renewability of the health insurance for parents in the policy wording. This feature ensures continued coverage regardless of age or claim history. It safeguards your parents from losing insurance support when healthcare needs peak later in life.

Coverage for Critical Illness

Some plans include built-in critical illness benefits. This helps manage high-cost treatments such as cancer, cardiac surgeries, or organ transplants. Including this cover reduces dependency on savings during prolonged or specialised treatments.

Insurer Support

Strong customer support matters during medical emergencies. Check for 24×7 claim assistance, dedicated managers, and responsive helplines. Efficient insurer support reduces delays, confusion, and stress when you need help the most.

*Standard T&C apply

Eligibility Criteria for Mediclaim Policy for Parents

Anyone who plans to buy the Bajaj General Senior Citizen Health Insurance plan should meet certain criteria. The table below highlights the eligibility criteria for a health insurance for parents:

Entry Age | 46 years to 70 years |

Policy Period | Annual policy |

Sum Insured | Multiple sum insured options between ₹50, 000 to ₹50 lakh |

Renewability | Lifelong renewability |

Quick Links

Diverse more policies for different needs

Insurance Samjho

Saving vs Medical Expenses

Is Health Insurance just an expense

MHCP EDGE +

Kitna Health Insurance Cover Enough Hai?

Home Insurance-All Risk Cover

Home Insurance-Long Term Cover

Home Insurance-No Content Declaration

Home Insurance-World Wide coverage

Take control of your digital security

Data Privacy Day | Bajaj General Insurance

Be Cyber Jagrook

Explore our articles

View all

Create your profile to unlock exclusive benefits.

- Customised plans that grow with you

- Proactive coverage for future milestones

- Expert advice tailored to your profile

What Our Customers Say

Cashless Claims

Excellent service for your mediclaim cashless customers during COVID. You guys are true COVID warriors, helping patients by settling claims during these challenging times.

Arun Sekhsaria

Mumbai

29th May 2021

Instant Renewal

I am truly delighted by the cooperation you have extended in facilitating the renewal of my Health Care Supreme Policy. Thank you very much.

Vikram Anil Kumar

Mumbai

27th Jul 2020

Quick Claim Settlement

Good claim settlement service, even during the lockdown, has enabled me to sell the Bajaj General Health Policy to more customers.

Prithbi Singh Miyan

Pune

27th Jul 2020

Instant Policy Issuance

Very user-friendly. I got my policy in less than 10 minutes.

Jaykumar Rao

Bhopal

25th May 2019

FAQs

Can I obtain health insurance if my parents have a pre-existing condition?

Yes, you may obtain a health insurance plan that covers pre-existing ailments. This will be subject to the waiting period offered under the plan. When buying health insurance for parents who have an existing illness, opt for a plan with a minimum waiting period.

Is there any age limit for purchasing health insurance for parents?

When buying health insurance policies for parents, there is an age limit on the various plans. However, the age criterion may vary from insurer to insurer.

Is a medical examination required for Parents' Health Insurance?

As per the parents' health insurance plan, one may require a pre-medical health check-up. However, this may vary from one insurance company to another.

Is it possible to include my parents in the current health insurance policy?

In case you have a family floater health insurance plan, you may include them in the circle of protection, provided they are less than 65 years of age. However, it is recommended to opt for a plan that is dedicated to their varying health care needs.

How can I make my parents' insurance coverage more comprehensive?

To enhance the coverage of the existing health insurance plan, during renewal, you may look at increasing the sum insured. You may also look at including add-ons to the base plan that fulfil the requirements.

Which health insurance plan is best for parents?

To choose the ideal parents' health insurance plan, it's important to analyse their needs. Once you understand the needs of the parents, you may look for health insurance plans online. Compare the features, benefits, and premiums to make an informed decision. It is recommended to opt for a high sum insured, as over time the ailment may increase. It's better to be safe than sorry.

Does medical insurance give tax benefits to parents?

A health insurance premium that is paid for any parent above 60 years of age is eligible to avail of tax benefits.

How do I purchase health insurance for my parents online?

The technological advancement and accessibility via the internet today have made everything so easy, convenient, and time-saving. If you are looking forward to buying a suitable plan, look for a health insurance policy online. Within a few clicks, you can easily know what the plan has to offer, compare the benefits, check the coverage and make a wise decision.

Is there any age restriction for parents' health insurance?

The Bajaj General Silver Health Plan offers coverage for individuals up to 70 years of age. The entry age for parents or senior citizens will differ, as per the insurance company. Hence, it is recommended to go through the policy carefully and check the age criterion.

Why should I choose an early health-care plan for my parents?

Age is one of the most important factors that affect health insurance premiums. As one ages, the premium may also increase. Therefore, it is suggested to buy health insurance for parents at an early age. This will help to keep the premium in check. However, when it comes to senior citizens, the insurance companies have a cap on the age limit. When buying the plan, ensure to read the policy wording carefully.

Is it possible to enrol my elderly parents in a family floater insurance plan?

You may include your parents in a family floater plan; however, they should be less than 65 years of age. The entry age criterion may vary from insurer to insurer.

What's the difference between health insurance for a family and health insurance for parents?

The key difference between family floater health insurance and senior citizen health insurance is the entry age criterion. With our health insurance for families, parents who are less than 65 years of age can avail themselves of it. On the contrary, health insurance for senior citizens offers coverage for individuals up to 75 years of age.

How much health insurance do my parents require?

Uncertainty never comes with prior notice. When it comes to securing the health of yourself and your family members, it is highly recommended to opt for a high sum insured. The health requirements of an individual differ at different stages of life. Compared to younger age, senior citizens are prone to risks and diseases.

Is it necessary for me to purchase separate health insurance for my parents?

It is suggested to choose a dedicated plan for your parents/ senior citizens. If you include your parent who is less than 65 years of age under a family health insurance plan, the premium increases. This may increase the burden on your finances. Moreover, due to the age gap between the parents and other dependents, there are chances that they may have a pre-existing ailment as well. This will also increase the overall health insurance premium.

How to get a physical copy of your Bajaj General Insurance?

Request a physical copy from the insurer or take a printout of the digital policy document received via email.

How do you go about filing a claim for your parents' health insurance?

Filing a health insurance claim is no longer a tedious task. At Bajaj General Insurance, we offer a convenient health insurance claim process. You can now register the claim, upload the required documents, and know its status in no time.

For a cashless health insurance claim, ensure to take treatment in any of the network hospitals. In case treatment is availed at a non-network hospital, initially, the insured needs to make the payment on their own. Once done, they can file for reimbursement and adhere to the process.

How do I go about renewing health insurance plans?

Don’t stress the small things in life! The easiest and quickest way to renew your life insurance policy is by doing it online. Topping up your health cover gives you freedom from worrying about heavy medical expenses.

How is the health insurance renewal premium calculated?

We know that reading through the ponderous terms and conditions section of a health insurance policy isn’t always easy. So, here is the quick answer. Your renewal premium is calculated based on your age and coverage. As always, you can put the power of compounding to good use by investing in health insurance as early as possible.

Can I renew my expired health insurance policy?

Yes, of course. Life can get really busy and even things as important as renewing your health insurance plan can get side-lined. With Bajaj General, we turn back the clock to give a grace period where you can renew your expired policy. For 30 days from the expiry date, you can still renew your health cover with ease. Now, you can run the race at yo

Can I renew health insurance online?

Absolutely! All you have to do to renew your health insurance is click or tap a few times! You can definitely renew health insurance policies online and also buy new policy for your family & friends click here to know more.

Will I be able to transfer my health insurance policy from another providers?

Yes, as per IRDAI regulations, insurance portability between providers is allowed. This also includes transfer of benefits like Cumulative Bonus and credits relating to waiting period for pre-existing diseases.

Popular Search

Why juggle policies when one app can do it all?

Download Bajaj General App!

With GST waiver, individual and family floater policies for health, personal accident, and travel insurance (on retail basis) are 18% cheaper from 22 September 2025. Secure what matters at an affordable price!